UK Fiance Visa Advice And Recommendation

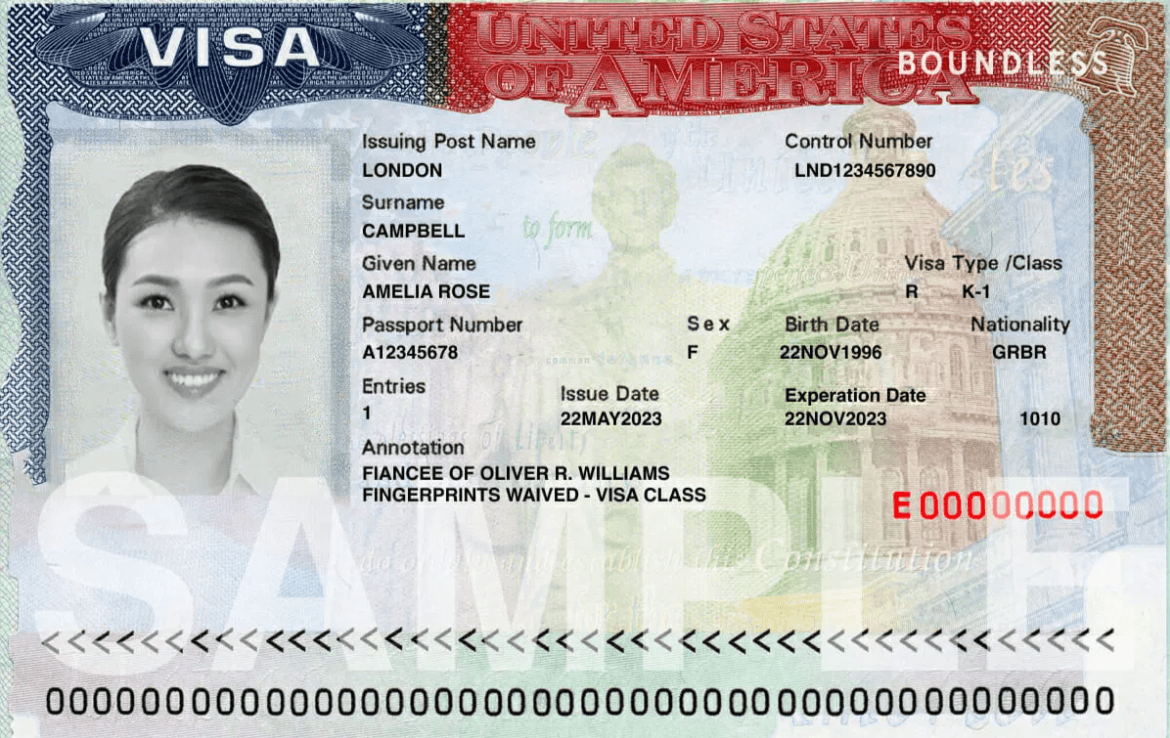

Do you have any plans to travel to the UK to meet and marry your fiancé? Although applying for a UK fiancé visa might be difficult and confusing, with the […]

Do you have any plans to travel to the UK to meet and marry your fiancé? Although applying for a UK fiancé visa might be difficult and confusing, with the […]

In today’s rapidly evolving business landscape, staying compliant with financial regulations is not just a necessity—it’s an imperative. These regulations, often intricate and multifaceted, serve as the backbone of financial […]

In a tough academic setting, students are supposed to perform excellently in exams and all academic tasks. Students often worry about their exams and class tests. The exam stress not […]

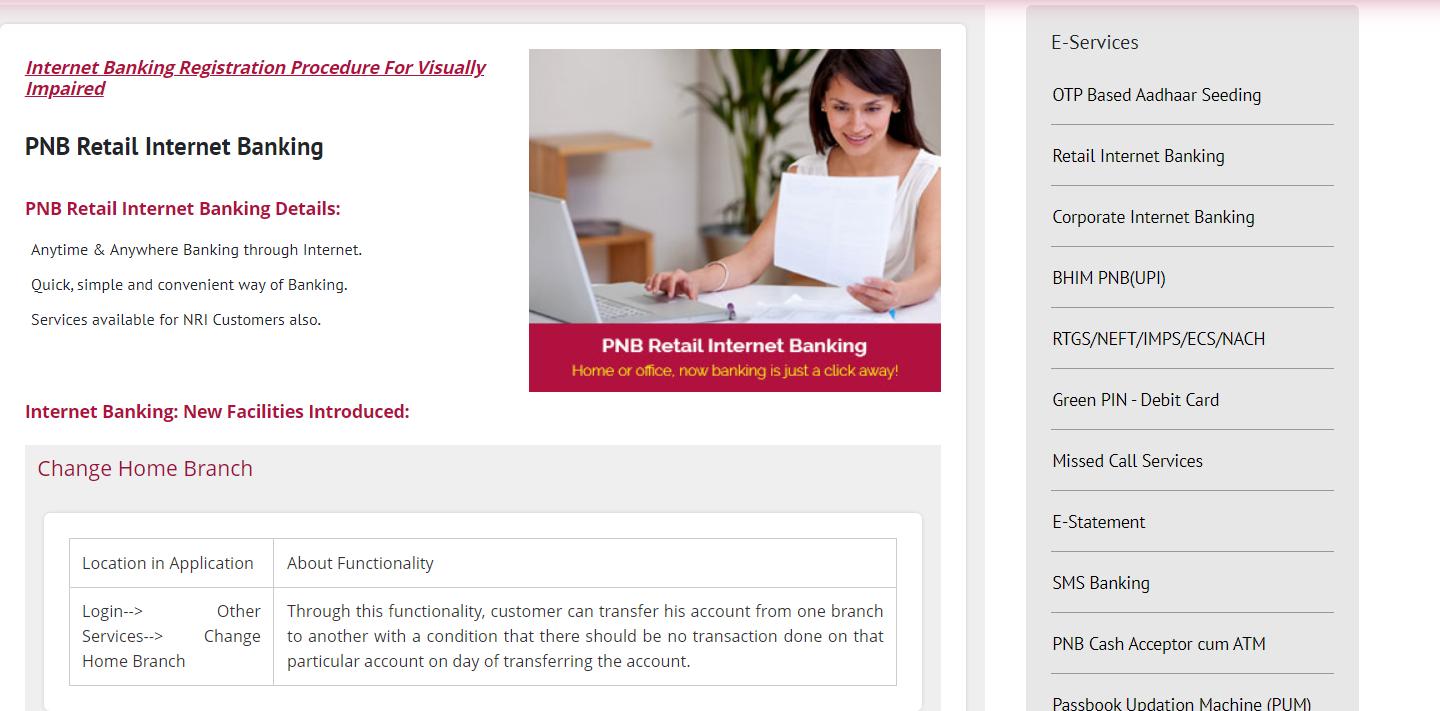

Punjab National Bank provides PNB Net Banking services to all its customers, allowing them to enjoy the advantages of online banking. When customers sign up for PNB internet banking, they […]

Trendzguruji.me is a learning platform that offers a variety of training opportunities for users. The site also provides industry information and podcasts. In addition, it facilitates interaction through virtual direct […]

What is the Airtel Mitra App? I will tell you all the information related to this APP in today’s article. Whatever questions you have in your mind, you will get […]

In this article, I am going to talk about few terms which are being used in The Indian Banking Sector & and those terminology are the Banking Ombudsman scheme of […]

Here is a compiled list of some of the top destination wedding venues in Rajasthan. 1. UDAIPUR Udaipur, the city of lakes, is the most romantic destination for weddings in […]

Airtel Payments Bank

In comparison to other betting sites, those with minimum deposit payments may help you if you’re a financially responsible gambler. The betting sites with the best 100 Rs deposit amounts […]